Determining The Ideal IUL Prospect

JULY 2018BY: JOHN HUTCHINSON

I’m often asked the question, “Who is the ideal candidate for indexed universal life and why?”

The world is full of opinions about letting investments be investments and that insurance should be strictly insurance and how IUL blurs these lines. However, it is the blurring between investments and insurance that makes IUL so attractive to certain types of people.

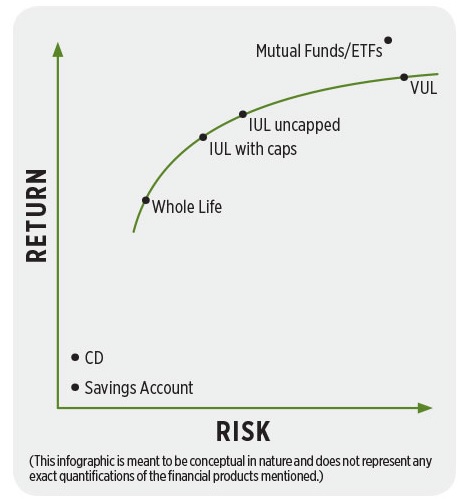

The fact that it’s possible to stay closer to the risk profile of a savings account with the opportunity to earn returns closer to the stock market is what makes IUL appealing as a piece of a broader balanced allocation strategy.

After all, who wouldn’t want the following benefits of IUL?

» Annual opportunities for double-digit growth without risk of market losses.

» Tax-sheltered growth and tax-exempt distributions.

» Guaranteed access to your equity without age restrictions.

» Protection against premature death (and possibly even severe illness or injury).

I believe it would be quite difficult — not to mention inefficient — to synthesize this same combination of benefits by cobbling together a medley of other financial products.

So who are the ideal prospects for IUL? Here are the types of people I’ve found to be enamored of IUL after they are properly educated about it.

Fiscally Responsible Families

The traditional paradigm of having affluent families maximize their retirement plans while struggling to pay off low-interest mortgage debt needs to be reexamined. From a tax-deduction standpoint, this combination of behaviors is often like having one foot on the gas and the other foot on the brake.

You’re eagerly maximizing one deduction, while aggressively trying to eliminate another. I could understand this mentality when interest rates were high, but the low hurdle rate of today’s mortgages may make it worthwhile to maintain this ongoing stream of payments while growing a bigger prudent reserve fund.

This is especially true if the vehicle’s long-term average growth rate doesn’t start with a decimal point, is sheltered from income tax and can be accessed without penalties before age 59 ½.

Don’t today’s families have just as many financial goals before retirement as they do during retirement?

If your client exhausts every precious drop of cash flow while aggressively paying down their mortgage and maxing out their 401(k) plans, won’t their liquidity profile look like that of someone living paycheck to paycheck?

I understand how lackluster savings accounts create a lost opportunity cost, but IUL gives your clients the unique ability to harness the power of tax-

sheltered growth while staying flush with liquidity and simultaneously protecting their family against catastrophic situations.

The best advice I could give to fiscally responsible families is to save money where they can safely send those dollars on a ride up the compound interest curve, without sacrificing access and control of their capital.

What’s interesting is that the major banks park more capital into performance-based life insurance policies (on the lives of their key executives) than they do into real estate, even though they have branches all over.

That’s why our company’s tag line is “Don’t do what banks say … do what they do.” Your clients also can reengineer permanent life insurance to act as their own private family bank.

Creating your clients’ own bank with a properly designed insurance policy can create unique financial opportunities that wouldn’t otherwise exist. What if your client wanted to partake in a capital-intensive business opportunity or pounce on a timely real estate deal? These opportunities would normally be available only to cash-rich investors, but IUL’s equity can be converted to cold, hard cash when these opportunities arise (without having to sacrifice growth while the client waits).

Entrepreneurs

Entrepreneurs often develop a love affair with IUL after they understand the many things it can do for them.

One of the features that make IUL so appealing is its completely flexible premium structure. Whole life insurance and term insurance have rigid premium schedules that can cause a policy to lapse if not strictly adhered to. With IUL, as long as you have positive cash surrender value, no mandatory premiums will be due.

Liquidity is the life-blood of an entrepreneur’s main wealth-building vehicle – their business. We find that entrepreneurs often keep large amounts of cash in nonperforming savings accounts simply because it must reside safely on-hand.

Remember that earlier in this article, I wrote that the biggest banks in America are diverting billions of their institutional reserves from low-yielding accounts into permanent life insurance policies on the lives of their key executives?

This big institutional thinking can easily be replicated by small and mid-sized business owners. IUL’s protection component is arguably more important for a local small business than it is for a Fortune 500 company. Losing an owner or a key employee can often mean the downfall of a small business, whereas it’s merely a speed bump for a huge corporation.

A properly structured IUL policy not only pays a tax-free death benefit, but also may provide certain “living benefits” if an owner or key employee becomes too sick or injured to keep working. These provisions may provide just enough tax-free cash to keep a business afloat long enough to get its bearings after losing one of its key people.

Not only that, but a company-owned policy can also simultaneously act as a supplemental retirement plan to recruit and retain these high-earning employees who need more than a 401(k) match to excite them. The policies owned by banks themselves are often tied to these types of “golden-handcuff” plans that simultaneously protect their human capital.

What Role Does IUL Play In Retirement?

Your clients may not need life insurance in retirement, but they certainly may want some. Here’s why.

I have found that the majority of Americans are over-allocated to the same stocks and mutual funds that lost half of their value not once, but twice from 2000 to 2010.

Now, I’m not saying your clients need to pull everything out of the market, but imagine that a portion of their retirement assets could still earn decent returns in good years but be immune from catastrophic declines. Your clients could feasibly draw funds strictly from their IUL policy cash value in these periods instead of redeeming a large number of shares from their stocks and mutual funds while they’re depressed in value.

This capacity to let a traditional portfolio heal is reason enough for your clients to start diversifying some of their retirement dollars toward IUL.

What about taxes in retirement? Can you think of a few reasons tax rates may go up in the future – for everyone? How about 21 trillion reasons and counting?

If all your clients’ assets are in taxable investments or tax-deferred retirement plans, how much control of their tax situation will they have in retirement?

What if, with the stroke of a pen, Congress raises tax rates on everyone to make up for the $21 trillion deficit? Is it coincidental that the amount of our national debt seems to track the amount of money that Americans hold in qualified retirement plans?

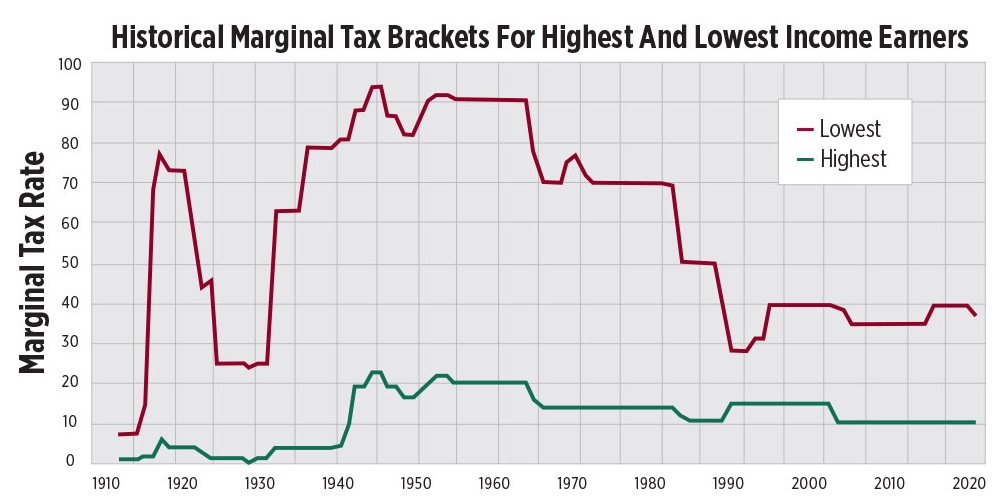

Take a look at how erratic our tax policy has been in the past.

Thankfully though, there always has been a sizable spread between the more reasonable lower tax brackets and the extremely penal higher brackets.

Amassing a sizable cash value balance inside an IUL policy by retirement could help your clients effectively toggle their tax situation from year to year as tax policy changes.

As long as your clients can keep just some amount of their death benefit in force (even if they bleed it down for income during retirement), then all of IUL’s tax-exempt distributions during their lifetime become permanently forgiven once that death claim is paid to any beneficiary.

So if tax rates suddenly become parabolic and your clients’ total taxable retirement income creeps into the unfavorable brackets, they could easily tighten the spigot from their individual retirement account or 401(k) account and supplement by taking tax-exempt income from their IUL policy so that they never reach those higher brackets.

In the most extreme cases of future tax hikes, your clients could completely scale back their taxable retirement withdrawals and aggressively pull from a heavily funded IUL policy. Once tax policy stabilizes or the pendulum swings back the other way, clients could then pull from their retirement plan assets to make their IUL whole again.

IUL has substantial utility when you think outside the box and don’t put IUL in the small corner that many financial pundits do.

Are there costs? Of course, but are the costs worth the unique benefits and planning possibilities that IUL provides? Ultimately you can be the judge of that, but we’ve found that the cost/benefit trade-off of a properly structured policy can be attractive once clients are properly educated.

So, who are the ideal candidates for IUL?

» Anyone who is concerned with the very real retirement risks of both violent volatility and massive tax hikes.

» People who need or want to keep excess liquidity safely on hand for long periods of time.

» Families or businesses that would be negatively impacted by someone who can no longer work because of death, chronic illness or severe injury.

It is unclear as to who exactly penned this fitting quote, but it applies perfectly to the divide between the reality and perception of IUL.

“There is a principle which is a bar against all information, which is proof against all arguments, and which cannot fail to keep a man in everlasting ignorance — that principle is contempt prior to investigation.”

— Unknown.

John “Hutch” Hutchinson is an independent insurance agent and registered investment advisor in San Clemente, Calif. He is founder of BankingTruths.com, an educational site for both consumers and advisors. He may be contacted at john.hutchinson@innfeedback.com.

John “Hutch” Hutchinson is an independent insurance agent in San Clemente, Calif. He is founder of BankingTruths.com, an educational site for both consumers and advisors to learn how to structure life insurance to act as their own private bank. Hutch may be contacted at john.hutchinson@innfeedback.com. john.hutchinson@innfeedback.com.