November 15, 2019

What is Fixed Annuities

What Is a Fixed Annuity?

A fixed annuity is a type of annuity contract that allows for the accumulation of capital on a tax-deferred basis. In exchange for a lump sum of capital, a life insurance company credits the annuity account with a guaranteed fixed interest rate while guaranteeing the principal investment. A fixed annuity can be annuitized to provide the annuitant with a guaranteed income payout for a specified term or for life.

How a Fixed Annuity Works

Insurance companies or financial institutions offer fixed annuities for a lump-sum payment (usually most of the annuitant’s cash and cash-equivalent savings), or they can be paid for on a periodic basis while the annuitant is still working. The money that is invested in the annuity is guaranteed to earn a fixed rate of return throughout the accumulation phase of the annuity (when money is being put into it).

Fixed annuities are contracts issued by life insurance companies to individuals looking for guaranteed rates of return without any risk to principal. Basically, steady, risk-free returns over a set period of time, for a fee. Because they are a type of insurance contract issued by a life insurance company, they enjoy some of the same tax benefits of life insurance policies, such as tax-deferred growth of earnings. Taxes are paid when the earnings are withdrawn or when the contract is annuitized for monthly payments.

During the annuitization phase (when money is being paid out), the balance invested, minus payouts, will continue to grow at this fixed rate. In some cases, however, annuitants don’t live long enough to claim the full amount of their annuities. When this happens, they usually end up passing the remainder of their annuity savings to the company that sold it to them. Whether the annuitant chooses to try to avoid this outcome depends on the kind of policy purchased.

When you are considering buying a fixed annuity, it is important to remember that you can often negotiate the price of these products. Also, the amount of money that an annuity will pay out varies (sometimes greatly) among the financial intermediaries selling them, so it’s best to shop around and avoid making quick decisions.

The two main types of fixed annuities are life annuities and term certain annuities. Life annuities pay a predetermined amount each period until the death of the annuitant, while term certain annuities pay a predetermined amount each period (usually monthly) until the annuity product expires, which may very well be before the death of the annuitant.

Benefits of a Fixed Annuity

Competitive Fixed Yields

The rates on fixed annuities are derived from the yield a life insurance company generates from its investment portfolio, which is invested primarily in high-quality corporate and government bonds. The yield on fixed annuities is typically higher than the yield on equivalent risk-free investments and is often guaranteed for a period of one to 10 years.

Tax-Deferred Growth

As a tax-qualified vehicle, fixed annuities offer tax-deferred accumulation of earnings. For people in the higher tax brackets, this can make a significant difference in the amount accumulated over time. When the earnings are withdrawn or taken as income, they are taxed as ordinary income. The amount paid in taxes is determined at that point by the annuitant’s current tax bracket.

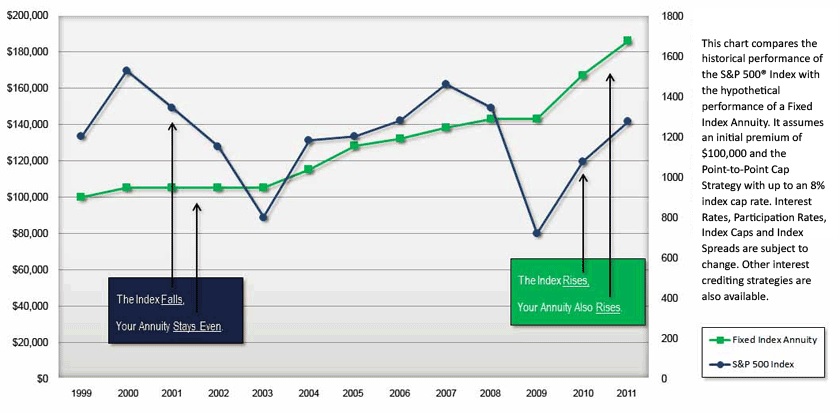

A Chart of Account

Below is a chart during the recession on what happens through a fixed index annuity or IUL (Index Universal Life)

Guaranteed Minimum Rates

Once the initial guarantee period expires, the rate is adjusted based on a specific formula or the prevailing yield earned in the insurer’s investment account. As a measure of protection against declining interest rates, fixed annuity contracts include a minimum rate guarantee.

Withdrawals

Fixed annuities allow for one annual withdrawal per year up to 10 percent of the account value. During the surrender period, which can run from one to 15 years from the start of the contract, withdrawals over 10 percent are subject to a surrender charge. The surrender charge declines each year until it reaches zero and withdrawals are free from this charge. Withdrawals made prior to age 59 ½ may be subject to a tax penalty of 10 percent in addition to ordinary income taxes.

Guaranteed Income Payments

Fixed annuities may be converted to an immediate annuity at any time to generate a guaranteed income payout for a specified period of time or for the life of the annuitant.

Safety of Principal

The life insurance company guarantees the capital invested in a fixed annuity. For that reason, investors should only consider investing with life insurance companies rated A or better for their financial strength.

Criticisms of Fixed Annuities

No investment is perfect, and this is also true of annuities. Any annuity requires you to give money to an insurance company for a period of time, during which you will not have access to it. Annuities can also carry hefty fees that eat into returns. Finally, annuities are not protected by any national insurance program. If the insurance company offering the annuity goes out of business, the annuitant may never recover the money.

The Bottom Line

Fixed annuities are a powerful vehicle for saving for retirement and guaranteeing regular streams of income during it. They are often used for tax deferral and savings. At the same time, annuities can be very tricky to manage for maximum returns, as the cost of insurance features can eat into the return on the initial investment.