December 10, 2019

What Is a

Section 1035 Exchange?

A 1035 exchange is a provision in the Internal Revenue Service (IRS) code allowing for a tax-free transfer of an existing annuity contract, life insurance policy, long-term care product, or endowment for another one of like kind. To qualify for a Section 1035 exchange, the contract or policy owner must also meet certain other requirements.

The IRS allows holders of these types of contracts to do this in order to replace outdated contracts with new contracts with improved benefits, lower fees, and different investment options.

Both full and partial 1035 exchanges are permitted, although some rules will vary by company. Typically, 1035 exchanges between products within the same company are not reportable for tax purposes as long as the IRS criteria for the exchange are satisfied.

Years after purchasing a annuity or life insurance policy, a policyholder might determine that the policy held might not be the best fit for his or her particular circumstances. This decision might be based on personal or economic reasons. In this case, the Internal Revenue Service (IRS) has created a 1035 Exchange to allow for the transfer of funds without incurring tax expenses.

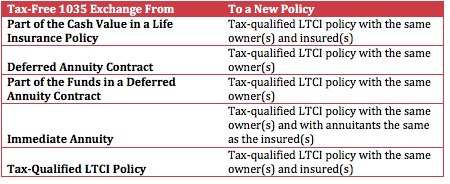

The following exchanges of insurance contracts are considered tax-free by the IRS:

- Replacing one annuity contract for another annuity contract with identical annuitants

- Replacing one life insurance policy for another life insurance policy, endowment policy or annuity contract

- Replacing one endowment policy for an identical endowment policy or an annuity contract

Any other variation from those acceptable exchanges listed above (annuity contract for life insurance) will not be considered a tax-free exchange. The IRS has provided strict guidelines that the owner, insured, and annuitant must be the same on the new contract as listed on the old in order to qualify for the tax-free treatment. The contract must also exchange directly between the insurance companies to retain the tax-free status. The IRS has ruled in several previous cases that if an owner cashes out of a current contract and immediately applies the proceeds to a new contract it will not be treated as a tax-free event or Section 1035 Exchange

How a Section 1035 Exchange Works

The primary benefit of a section 1035 exchange is that it lets the contract or policy owner trade one product for another with no tax consequence. That way, they can exchange outdated and underperforming products for newer products with more attractive features, such as better investment options and less restrictive provisions.

Additionally, a section 1035 exchange lets policyholders preserve their original basis, even if there are no gains to be deferred. For example, Joe Sample invested a total of $100,000 (cost basis) in a non-qualified annuity and subsequently took no loans or withdrawals. But because of poor investment performance, its value dropped to $75,000. Dissatisfied, Joe decided to transfer his funds into another annuity with another company. In this scenario, the original contract’s cost basis of $100,000 becomes the new contract’s basis although just $75,000 was transferred.

Despite the tax benefits, 1035 exchanges do not absolve contract owners of their obligations under the original contract. For example, insurance companies typically don’t waive surrender charges for 1035 exchanges. However, if the owner exchanges one product for another within the same company, the fees may be waived.